The ADU Revolution: New Fannie Mae Rules Unlock More Income and More Units

For years, homeowners and investors looking to maximize their property’s potential were often limited by rigid financing rules. If you wanted to build an Accessory Dwelling Unit (ADU) or use the rent from one to qualify for a mortgage, the path was narrow.

That has officially changed. Thanks to recent updates to the Fannie Mae Selling Guide, there are now powerful new options for both standard “conventional” financing and HomeStyle Renovation loans.

1. Use ADU Rent to Qualify for Your Mortgage

Historically, it was difficult to count “projected” rent from a unit that hadn’t been built yet. Now, Fannie Mae allows you to utilize projected rental income for qualification on a HomeStyle Renovation loan.

Because these loans use the “as-completed” appraised value, the appraiser can also provide an “as-completed” rent schedule (using Form 1007 or 1025). This allows you to count that future income toward your debt-to-income (DTI) ratio today.

Key Requirements:

- Income Cap: The ADU income used cannot exceed 30% of your total qualifying income.

- The 75% Rule: Only 75% of the projected gross rent is used, providing a 25% buffer for vacancies and maintenance.

- Eligible Transactions: This applies to purchases and limited cash-out refinances.

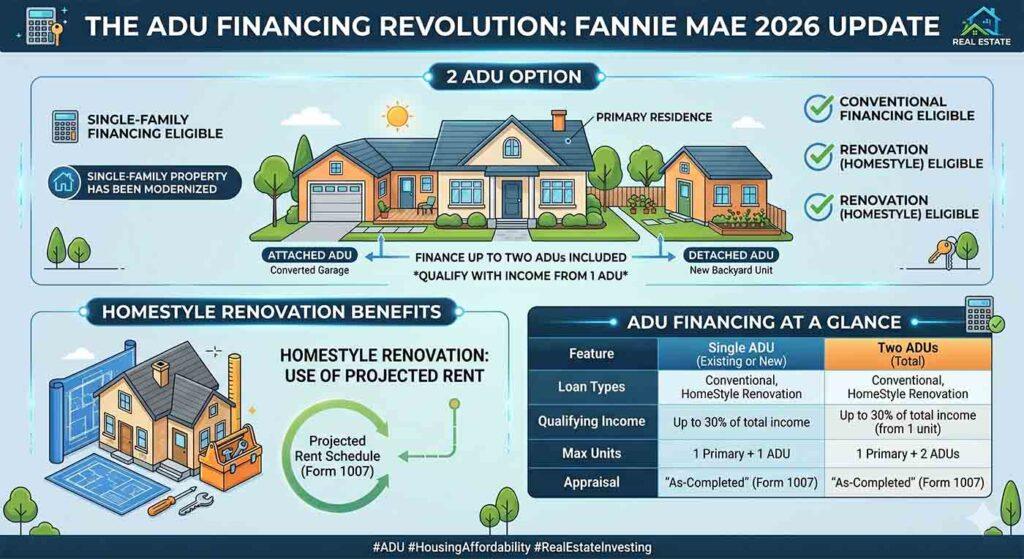

2. Breaking the “One ADU” Barrier: Finance Up to Two ADUs

The biggest breakthrough in the latest 2026 update is the expansion of property eligibility. Previously, Fannie Mae would typically only recognize one ADU on a single-family property.

Now, you can finance properties with up to TWO ADUs:

- Standard Conventional & Renovation: Eligibility now extends to one-unit properties with up to two ADUs.

- Multi-Unit Expansion: For 2-to-3 unit properties, you can now include ADUs as long as the total number of units (primary units + ADUs) does not exceed four.

- Rental Income Note: While you can now finance a property with multiple ADUs, current qualifying rules generally still limit the rental income used for qualification to be derived from only one of those ADUs.

Graphics: ADU Financing at a Glance

Feature | Single ADU (Existing or New) | Two ADUs (Total) |

Loan Type | Conventional / HomeStyle | Conventional / HomeStyle |

Qualifying Income | Up to 30% of total income | Up to 30% (from 1 unit) |

Appraisal Method | “As-Completed” (Form 1007) | “As-Completed” (Form 1007) |

Max Units | 1 Primary + 1 ADU | 1 Primary + 2 ADUs |

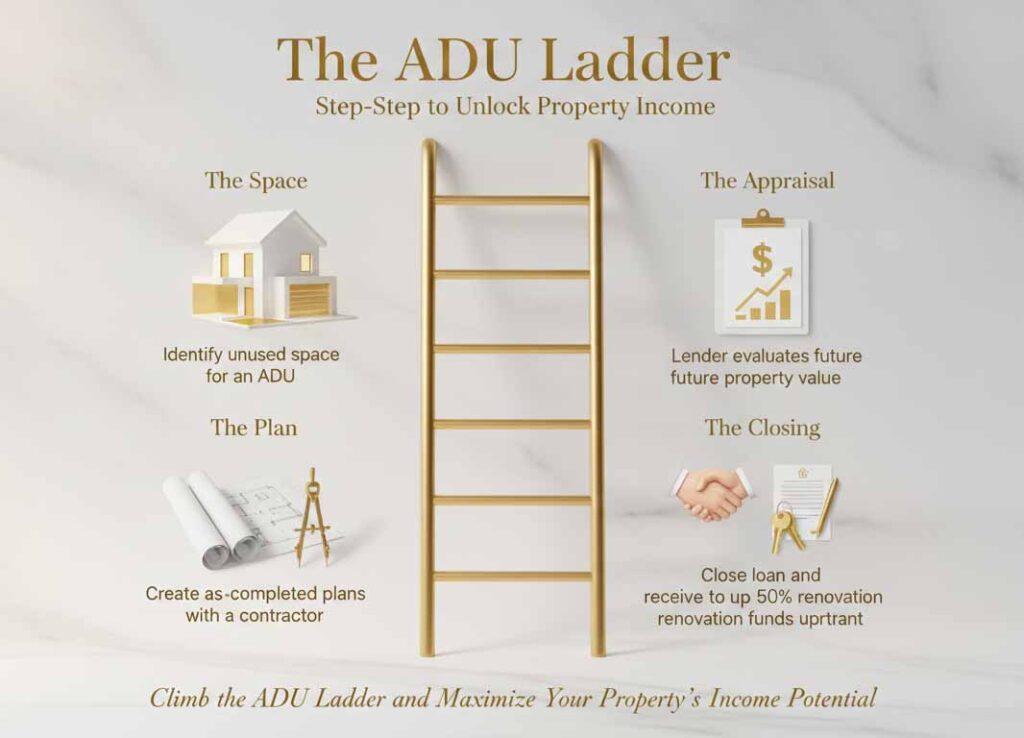

- Step 1: The Space. Identify a basement, garage, or backyard area.

- Step 2: The Plan. Work with a contractor to get “as-completed” specs.

- Step 3: The Appraisal. Your lender orders an appraisal that values the home after the ADUs are built.

- Step 4: The Closing. Close on your loan and get up to 50% of renovation costs disbursed immediately to start construction.

Why This Matters

Whether you are looking to house a multi-generational family or create a “house hacking” investment strategy, these rules provide the flexibility to make it happen. By allowing two ADUs, Fannie Mae is aligning with many new state and local laws (like those in California) that have legalized “triplex” style living on single-family lots.

Ready to start your ADU project or have any questions?